ESRS Set 2: Revising CSRD Reporting Standards

After a first year of reporting based on the ESRS “Set 1”, the European Commission has once again mandated EFRAG to revise the standards.

The objective is clear: simplify the framework, reduce the volume of data and make reporting more operational for companies.

But have these goals been achieved?

Early feedback remains mixed.

Lower ambitions for CSRD

A widely shared conclusion is emerging: the initial ambitions of CSRD have been scaled back. This shift moves away from the transparency objectives originally promoted under the European Green Deal.

On 13 November 2025, the European Parliament adopted a proposal to significantly raise the applicability thresholds to 1,750 employees and €450 million in revenue.

If confirmed, this change could drastically reduce the number of companies subject to CSRD across Europe – by up to 90%.

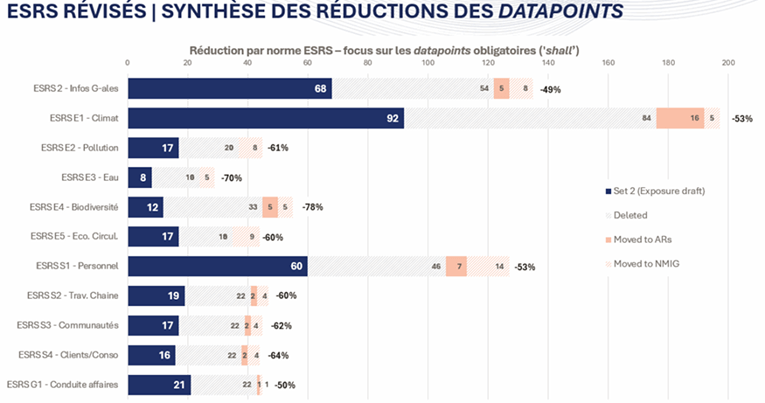

Fewer data points, greater clarity

At the same time, ESRS Set 2 introduces a significant reduction in mandatory data points. Depending on the standard, reductions could reach between 50% and 80%.

Some topics are particularly affected. For example, water (ESRS E3) and biodiversity (ESRS E4) would be reduced to only a limited number of mandatory data points.

This reflects a clear intention to simplify. However, it also raises an important question: does simplification come at the expense of ambition?

A rationalisation of ESRS standards

Alongside this reduction, EFRAG has worked to clarify the standards. The language has been simplified, and the structure of the texts has been improved. Complex topics such as double materiality are now easier to understand.

Redundant or overly complex data points have been removed. Most importantly, the distinction between mandatory requirements and methodological guidance is now clearer. The goal is to make the standards more accessible and more operational for reporting teams.

What Set 2 changes in practice

Beyond the intention to simplify, ESRS Set 2 introduces several structural changes.

First, mandatory requirements are now clearly identified within the main body of the standards.

Second, methodological elements are grouped separately. Optional data points are removed and replaced by non-binding recommendations.

In addition, the structure of the standards has evolved. The distinction between “Disclosure Requirements” and “Application Requirements” is more explicit.

Complementary methodological guidance, the “Non-Mandatory Illustrative Guidance”, provides additional support without being legally binding. The result is a framework that is easier to navigate, but still demanding.

Focus: the ESRS S1 example

The ESRS S1 standard provides a clear illustration of this simplification process. More than half of the mandatory data points have been removed.

Certain requirements have also been eased. For instance, disclosures related to non-employee workers are now optional, unless deemed material.

At the same time, thresholds have been clarified and key indicators standardised to improve comparability across reports. However, this simplification does not reduce the need for structured and reliable data.

Auditors call for caution

In this evolving context, auditors are urging companies to remain cautious. Simplifying the standards should not lead to reduced efforts.

Data collection and reliability remain critical challenges. Companies must continue strengthening internal controls, documenting processes and improving data quality.

For organisations already subject to CSRD, audits will continue to rely on existing standards. For those preparing, double materiality remains a key step.

Structuring ESG data remains essential

Despite ongoing changes, one constant remains: the ability to structure ESG data is central. Simplifying the standards does not eliminate operational complexity.

Data collection, consolidation and traceability remain key challenges. Companies that invest in robust data structures will be better equipped to adapt to future regulatory changes.

CSRD software as a strategic lever

In this context, tools become a strategic enabler. CSRD software helps centralise data, ensure reliability and secure reporting processes. But the challenge goes beyond compliance.

The objective is to build a scalable foundation that can evolve with regulatory changes without requiring a complete overhaul of processes.

Sustainability reporting is no longer just about producing a report — it becomes a management system.

What comes next?

At the European level, the legislative process is ongoing. The trilogue between the Commission, the Council and the Parliament is expected to conclude by the end of the year.

EFRAG is also expected to submit its technical advice on the revised standards in the coming weeks. In this shifting environment, companies must move forward without waiting.

Key takeaways

ESRS Set 2 does not represent a break, but a shift. Less ambitious in volume, more pragmatic in structure, it reshapes ESG reporting without fundamentally changing its core requirements.

In this context, one priority remains: producing reliable, auditable and actionable data.A key challenge for both compliance and strategic decision-making.